Today, cryptocurrency, led by Bitcoin, Litcoin, Ether, etc. are taking the financial world by storm as more people invest and buy these currencies.

Despite its growing popularity governments are cracking down on the digital currency because it is decentralized, meaning it has no central authority in the way the Indian government holds authority over the Rupee or Dollar. Therefore, some experts believe crypto poses a threat to central banks and national security.

So, what are its pros and cons? But, before we learn about its major advantages and disadvantages let us decode what are Cryptocurrencies. Without further ado, let’s begin.

Crypto-currency is a form of payment that can be exchanged online for goods and services.

Many companies have issued their own currencies, often called tokens, and these can be traded specifically for the good or service that the company provides. Think of them as you would arcade tokens or casino chips. You’ll need to exchange real currency for the cryptocurrency to access the good or service.

Cryptocurrency is completely in the cloud, it does not attain a physical form but have a digital value, and can be used for digital equivalent of cash in a steadily increasing number of retailers and other businesses. Bitcoin was the first cryptocurrency that was ever created.

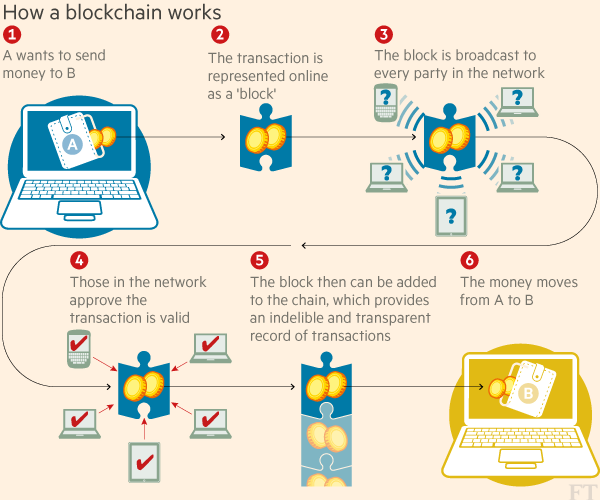

Cryptocurrencies work using a technology called blockchain. Blockchain is a decentralized technology spread across many computers that manages and records transactions.

So, instead of relying on traditional financial institutions like RBI who verify and guarantee your transactions, cryptocurrency transactions are verified by the user's computers logged into the currency's network.

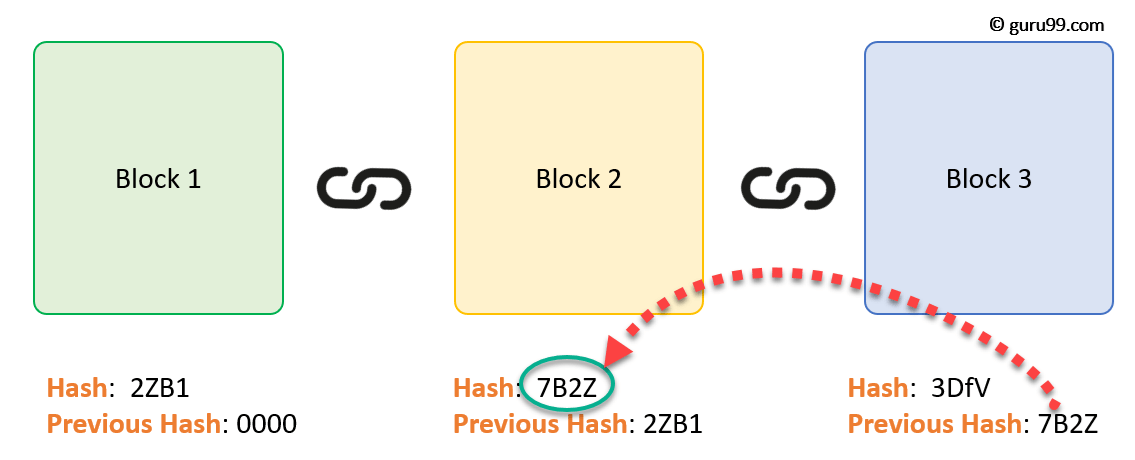

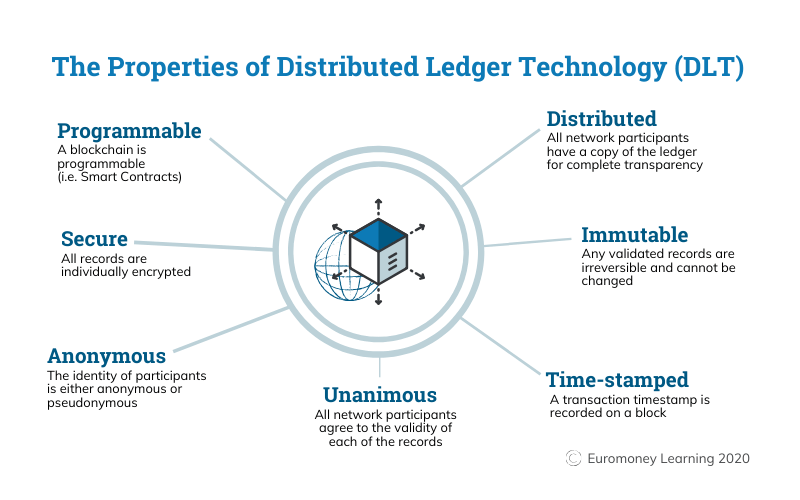

Getting the concepts right!Blockchain TechnologyBlockchain is a system of recording information in a way that makes it difficult or impossible to change, hack, or cheat the system. A blockchain is essentially a digital ledger of transactions that is duplicated and distributed across the entire network of computer systems on the blockchain. Each block in the chain contains a number of transactions, and every time a new transaction occurs on the blockchain, a record of that transaction is added to every participant’s ledger. The decentralised database managed by multiple participants is known as Distributed Ledger Technology (DLT). Blockchain is a type of DLT in which transactions are recorded with an immutable cryptographic signature called a hash. Watch this video for better understanding: https://youtu.be/SSo_EIwHSd4

Blockchain is a chain of blocks that contain data

What is Cryptocurrency Mining?Cryptocurrency mining is the process in which transactions between users are verified and added to the blockchain public ledger. The process of mining is also responsible for introducing new coins into the existing circulating supply and is one of the key elements that allow cryptocurrencies to work as a peer-to-peer decentralized network, without the need for a third party central authority. Watch this video for better understanding: https://youtu.be/2VtH-XAOjXw

|

![]()

Transparency

In the trading of cryptocurrency, each and every transaction is recorded on the blockchain. The blockchain keeps the information about everything. If at any point in time, anyone has publicly used the address of cryptocurrency, then anyone can see that how much crypto that person is owned. This means that the data is available to view by anyone at any time, and that’s a major boon for those wishing for a more transparent banking system or financial system.

Self-governed and managed

Governance and maintenance of any currency is a major factor for its development. The cryptocurrency transactions are stored by developers/miners on their hardware, and they get the transaction fee as a reward for doing so. Since the miners are getting paid for it, they keep transaction records accurate and up-to-date, keeping the integrity of the cryptocurrency and the records decentralized.

Easily Accessible Across the Globe

As of now, Cryptocurrencies are easily and readily available to all its users. It is simply a decentralized system of currency which can be accessed across the globe.

Low Operation Cost

One of the major uses of cryptocurrencies is to send money across borders. With the help of cryptocurrency, the transaction fees paid by a user are reduced to a negligible or zero amount. It does so by eliminating the need for third parties, like VISA or PayPal, to verify a transaction. This removes the need to pay any extra transaction fees.

Reduced Remittance

Many governments around the world are implementing isolationist policies which restrict remittances made from other countries by making the charges too high or by writing new regulations. This fear of not being able to send money to family members and others is driving more people towards digital Cryptocurrency, chief amongst them being Bitcoin.

Protection from inflation

Inflation has caused many currencies to get their value declined with time. Almost every cryptocurrency, at the time of its launch, is released with a fixed amount. The source code specifies the amount of any coin; like, there are only 21 million Bitcoins released in the world. So, as the demand increases, its value will increase which will keep up with the market and, in the long run, prevent inflation.

Absolute Anonymity

Cryptocurrency is completely anonymous, which is great for those that value their online privacy and are wary of handing over too much of their digital data. For more law-abiding citizens, the benefits of anonymity are many. There is no chance of identity theft, and that’s of major interest to anyone looking for more secure ways to remain online safely.

Instant and 24-hour accessibility

It is possible to spend or buy wherever you are. Everything can be managed on your mobile device. This accessibility is a key feature for the adoption of bitcoin, and is being used across the world to provide opportunities for those who would previously have struggled to become online consumers.

Currency exchanges can be done easily

Cryptocurrency can be bought using many currencies like the US dollar, European euro, British pound, Indian rupee or Japanese yen. With the help of different cryptocurrency wallets and exchanges, one currency can be converted into the other by trading in cryptocurrency, across different wallets, and with minimal transaction fees.

Decentralized

The decentralization helps keep the currency monopoly free and in check so that no one organization can determine the flow and the value of the coin, which, in turn, will keep it stable and secure, unlike fiat currencies which are controlled by the government.

Secure and private

The blockchain ledger is based on different mathematical puzzles, which are hard to decode. This makes a cryptocurrency more secure than ordinary electronic transactions. Cryptocurrencies, for better security and privacy, use pseudonyms that are unconnected to any user, account or stored data that could be linked to a profile.

Unlimited Transactions

With the help of a crypto wallet, you can pay anyone, any amount and anywhere, there is no restriction on sending limit. The transaction cannot be prevented or controlled, so you can make transfers across the globe wherever another user with a cryptocurrency wallet is located.

Volatile since unregulated

Cryptocurrencies are much more prone to volatility. Cryptocurrencies are digital asset, not usually backed by a physical commodity or currency. This means that their value is completely dependent on faith.

Their price follows the laws of supply and demand. In the absence of regulatory oversight, market manipulation can occur, which introduces volatility. This, in turn, discourages institutional investment in the market. Thus, a cryptocurrency may be a worth of a fortune today in the market and be utterly worthless tomorrow.

Can be used for illegal transactions

Since the privacy and security of cryptocurrency transactions are high, it’s hard for the government to track down any user by their wallet address or keep tabs on their data. Bitcoin has been used as a mode of exchanging money in a lot of illegal deals in the past, such as buying drugs on the dark web. Cryptocurrencies are also used by some to convert their illicitly obtained money through a clean intermediary, to hide its source.

Data losses can cause financial losses

The developers wanted to create virtually untraceable source code, strong hacking defenses, and impenetrable authentication protocols.

This would make it safer to put money in cryptocurrencies than physical cash or bank vaults. But if any user loses the private key to their wallet, there’s no getting it back. The wallet will remain locked away along with the number of coins inside it. This will result in the financial loss of the user.

Decentralized but still operated by some organization

The cryptocurrencies are known for its feature of being decentralized. But, the flow and amount of some currencies in the market are still controlled by their creators and some organizations. These holders can manipulate the coin for large swings in its price. Even hugely traded coins are susceptible to these manipulations like Bitcoin, whose value doubled several times in 2017.

Some coins not available in other fiat currencies

Some cryptocurrencies can only be traded in one or a few fiat currencies. This forces the user to convert these currencies into one of the major currencies, like Bitcoin or Ethereum first and then through other exchanges, to their desired currency. This applies to only a few cryptocurrencies. By doing this, the extra transaction fees are added in the process, costing unnecessary money.

No refund or cancellation policy

If there is a dispute between concerning parties, or if someone mistakenly sends funds to a wrong wallet address, the coin cannot be retrieved by the sender. This can be used by many people to cheat others out of their money. Since there are no refunds, one can easily be created for a transaction whose product or services they never received. There is no involvement of banking institutions making it a drawback.

Not Accepted Across All Vendors

Cryptocurrency is only accepted by the few vendors. Between that and fluctuation in prices, all the money which are saved in the cost of transactions could be negligible

Absolute Anonymity

The black market and the dark web are big users of cryptocurrency. Terrorists and criminals would value their anonymity for making transactions that are virtually untraceable.

Susceptible to hacks

Although cryptocurrencies are very secure, exchanges are not fully secure. Most exchanges store the wallet data of users to operate their user ID properly. This data can be stolen by hackers, giving them access to a lot of accounts.

After getting access, these hackers can easily transfer funds from those accounts. Some exchanges, like Bitfinex or Mt Gox, have been hacked in the past years and Bitcoin has been stolen in thousands and millions of US dollars. Most exchanges are highly secure nowadays, but there is always a potential for another hack.

Cryptocurrencies are not legal tender in India, and while exchanges are legal. However there are many countries like America investing in cryptocurrencies and making it legal.

The RBI, in its wisdom to protect the interests of the country, had virtually banned cryptocurrency trading in India through its circular issued on April 6, 2018.

The sweeping regulation prohibited trade of cryptocurrencies on domestic exchanges.

The Supreme Court in 2020 however quashed the order by the Reserve bank of India (RBI) banning financial services firms from trading in virtual currency or cryptocurrency.

The Indian government has issued repeated warnings against investing in digital currencies, saying these were like Ponzi schemes that offer unusually high returns to early investors.

The government has prepared a draft bill that seeks to prohibit mining, holding, selling, trade, issuance, disposal or use of cryptocurrency in the country.

Under the draft bill, all the aforementioned activities can be punished with a fine or imprisonment up to 10 years, or both in some cases.

International ExamplesU.S.A Draft ‘Cryptocurrency Act of 2020’ defines cryptocurrencies into categories namely, crypto-commodities, crypto-securities and crypto- currencies. This is done in order to assign the appropriate federal crypto regulator as a soul government agency with authority to regulate: Crypto-commodities (Agency-CTFC) Crypto-securities (Agency-SEC) Crypto-currencies (Agency-FinCEN) Each of the above federal crypto regulators is required to make available to the public a current list of all federal licenses, certifications, or registrations required to create or trade in all digital assets. The Act also mandates to establish rules similar to financial institutions on the ability to trace cryptocurrency transactions. Singapore The Singapore Government has not defined virtual currency. In this regard a new piece of legislation the “Payment Service Act” has been enacted. The PSA when enforced will regulate the purchase and sales of virtual currencies. However, this Act has not defined either cryptocurrency or virtual currency. It has used the term “Digital Payment Token” |

The Government can bring the crypto exchanges and other providers under the Prevention of Money Laundering Act, under the reporting entities in which case they will be treated same as banks, stock exchanges, intermediaries etc.

As they will follow all KYC measures and for this an amendment is not required and it can be done by a government notification which is the lowest hanging fruit.

© 2025 iasgyan. All right reserved