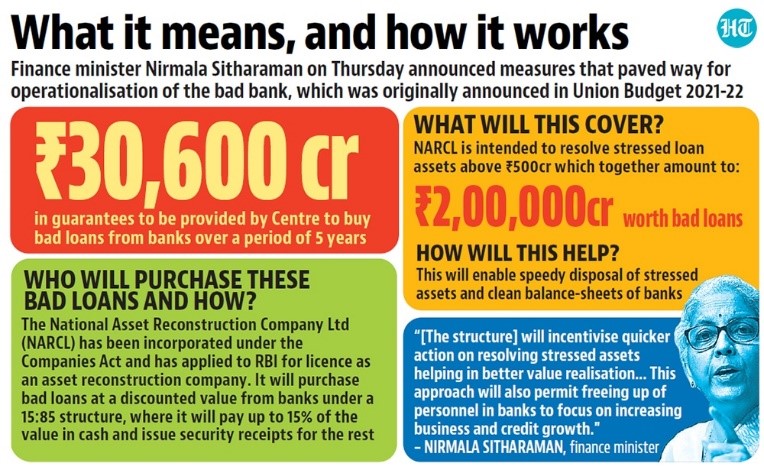

Government has announced “National Asset Reconstruction Company Limited” (NARCL) has already been incorporated under the Companies Act.

Details of the Announcement:

It will acquire stressed assets worth about Rs 2 lakh crore from various commercial banks in different phases.

Another entity — India Debt Resolution Company Ltd (IDRCL), which has also been set up — will then try to sell the stressed assets in the market.

The NARCL-IDRCL structure is the new bad bank.

To make it work, the government has okayed the use of Rs 30,600 crore to be used as a guarantee.

About Bad Bank

It’s an entity where all the bad loans from all the banks can be parked — thus, relieving the commercial banks of their “stressed assets” and allowing them to focus on resuming normal banking operations, especially lending.

While commercial banks resume lending, the so-called bad bank, or a bank of bad loans, would try to sell these “assets” in the market.

The bad bank structure will assist in consolidation of debt, currently fragmented across various lenders, thus leading to faster, single-point decision making, including through Insolvency and Bankruptcy Code (IBC) processes

Working Mechanism:

The NARCL will first purchase bad loans from banks.

It will pay 15% of the agreed price in cash and the remaining 85% will be in the form of “Security Receipts”.

When the assets are sold, with the help of IDRCL, , the commercial banks will be paid back the rest.

If the bad bank is unable to sell the bad loan, or has to sell it at a loss, then the government guarantee will be invoked and the difference between what the commercial bank was supposed to get and what the bad bank was able to raise will be paid from the Rs 30,600 crore that has been provided by the government.

A 15 percent cash payment will be made to banks for their toxic assets, 85 percent will be security receipts. There will be a backstop guarantee for the banks,

Government guarantee will be invoked to cover the shortfall between the amount realised from the underlying assets and the face value of SRs issued for that asset, subject to overall ceiling of ₹30,600 crore, valid for 5 years.

Positives :

A bank will get rid of all its toxic assets, which were eating up its profits, in one quick move.

When the recovery money is paid back, it will further improve the bank’s position. Meanwhile, it can start lending again.

the decision is in keeping with the government’s commitment to reduce non-performing assets (NPAs) of public sector banks (PSBs) through the four “R” strategy -- Recognition, Resolution, Recapitalisation and Reform.

Since the guarantee is in a form of contingent liability, it will not lead to immediate cash outflow and therefore is unlikely to impact the fiscal position in near future. It will boost the economic growth.

It will incentivise quicker action on resolving stressed assets, thereby helping in better value realization.

The five-year limit will encourage banks to not drag the process, adding NARCL has already been incorporated as a company.

Challenges:

The plan of bailing out commercial banks will collapse if the bad bank is unable to sell such impaired assets in the market.

Taxpayer Money to improve Banking: whether it is recapitalising PSBs laden with bad loans or giving guarantees for security receipts, the money is coming from the taxpayers’ pocket. While recapitalisation and such guarantees are often designated as “reforms”, they are band aids at best.