Description

Copyright infringement not intended

Picture Courtesy: moneycontrol.com

Context: The Reserve Bank of India (RBI) issued a directive instructing credit information companies (CICs) to develop a common Data Quality Index (DQI) specifically for the commercial and microfinance segments. This directive comes as part of the central bank's efforts to enhance the quality of data submissions made by credit institutions (CIs) to CICs, with the ultimate goal of improving data quality over time.

Details

- The RBI emphasized in its press release that the Data Quality Index (DQI) is a crucial tool for evaluating the accuracy, completeness, and reliability of data provided by credit institutions. By assessing data quality, it becomes possible to identify areas that require improvement, ultimately ensuring that the information reported to credit bureaus remains consistent and dependable.

Credit Information Company (CIC)

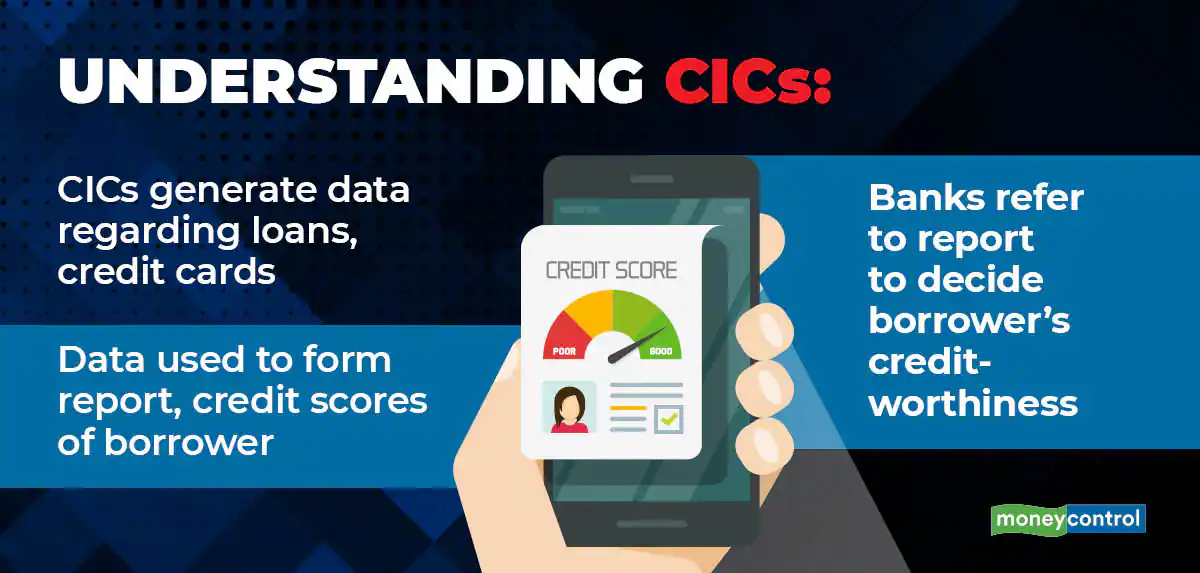

- A Credit Information Company (CIC) is a crucial component of the financial ecosystem in India, functioning as an independent third-party agency responsible for the collection and management of financial data related to individuals' loans, credit cards, and other pertinent financial information. This data is then shared with CIC members, who are typically banks and other financial institutions.

- Formation and Registration: A Credit Information Company must be established as a company and registered under the Companies Act, 1956. To operate legally, a CIC must obtain a Certificate of Registration as per sub-section (2) of Section 5 of the CIC Act, 2005.

- Regulation and Oversight: All Credit Information Companies in India are subject to regulation by the Reserve Bank of India (RBI).

- The CIC Act, 2005, clearly prohibits any entity from engaging in the business activity of credit information without obtaining the requisite Certificate of Registration from the RBI.

- CICs must adhere to the provisions laid out in the Credit Information Companies Regulation Act (CIC Act), 2005, as well as other guidelines and regulations set by the RBI.

- The Credit Information Companies, Regulations, and Rules Act, 2006, supplements the regulatory framework governing CICs.

- Data Collection and Sharing: CICs receive financial data from their member banks and other financial institutions. The data encompasses information regarding loans, credit cards, and related financial activities.

- Credit Information Reports and Credit Scores: Utilizing the collected data, a Credit Information Company compiles Credit Information Reports (CIR) and calculates Credit Scores for individual consumers. These reports and scores provide a comprehensive overview of an individual's credit history and financial behaviour.

- Data Classification: Credit history data of individuals is categorized by CICs into two primary segments: Negative data and Positive data.

- Negative data may encompass instances of late payments, defaults, or other adverse credit events.

- Positive data comprises records of punctual payments and responsible credit management.

- Presently, four licensed Credit Information Companies are operating in India: Credit Information Bureau (India) Ltd (CIBIL), Equifax Credit Information Services Pvt Ltd, Experian Credit Information Company of India Pvt Ltd, CRIF High Mark Credit Information Services Pvt Ltd.

Summary

- These CICs are integral to the Indian financial landscape, enabling responsible lending practices, aiding in risk assessment, and promoting financial inclusion by providing accurate and reliable credit information to lenders and financial institutions.

|

PRACTICE QUESTION

Q. Consider the following statements:

Statement 1: The primary function of a Credit Information Company (CIC) is to grant loans to individuals and businesses.

Statement 2: The Data Quality Index (DQI) is used by CICs to evaluate the accuracy of data provided by credit institutions.

Which one of the following is correct in respect of the above statements?

A) Both Statement-1 and Statement-2 are correct and Statement-2 is the correct explanation for Statement-1

B) Both Statement-1 and Statement-2 are correct and Statement-2 is not the correct explanation for Statement-1

C) Statement-1 is correct but Statement-2 is· incorrect

D) Statement-1 is incorrect but Statement-2 is correct

Answer: D

Explanation:

Statement-1 is incorrect because CICs do not grant loans; they collect and manage financial data.

Statement-2 is correct; the DQI is indeed used by CICs to assess data accuracy.

|

https://www.moneycontrol.com/news/business/rbi-directs-credit-information-companies-to-prepare-index-for-commercial-microfinance-segments-11398411.html