Description

Disclaimer: Copyright infringement not intended.

Context

- Ahead of the plenary session of the Financial Action Task Force, Pakistan is hoping to get its name removed from the FATF’s ‘grey list’.

What is the FATF?

- The Financial Action Task Force is an international watchdog for financial crimes such as money laundering and terror financing.

Establishment

- It was established at the G7 Summit of 1989 in Paris to address loopholes in the global financial system after member countries raised concerns about growing money laundering activities.

- In the aftermath of the 9/11 terror attack on the U.S., FATF also added terror financing as a main focus area. This was later broadened to include restricting the funding of weapons of mass destruction.

Members and meetings

- The FATF currently has 39 members. The decision-making body of the FATF, known as its plenary, meets thrice a year.

- Its meetings are attended by 206 countries of the global network, including members, and observer organizations, such as the World Bank, some offices of the United Nations, and regional development banks.

Mandate

- The FATF sets standards or recommendations for countries to achieve in order to plug the holes in their financial systems and make them less vulnerable to illegal financial activities.

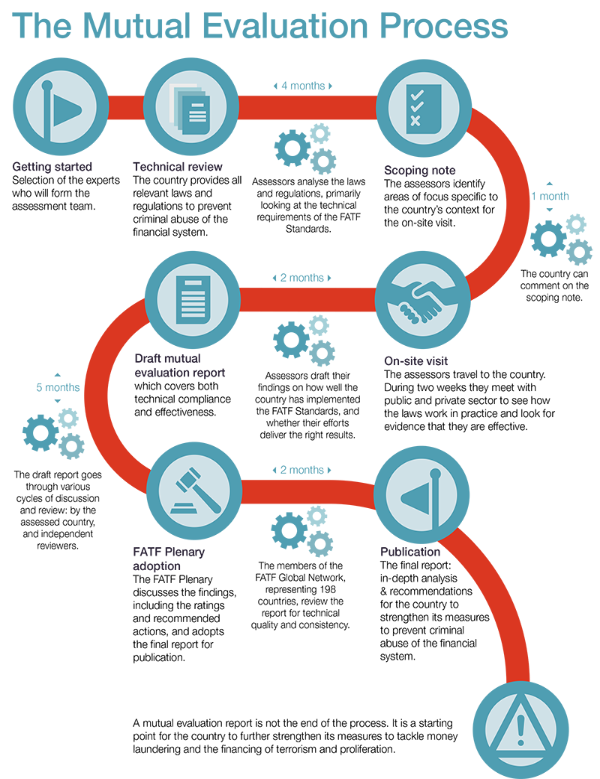

- It conducts regular peer-reviewed evaluations called Mutual Evaluations (ME) of countries to check their performance on standards prescribed by it. The reviews are carried out by FATF and FATF-Style Regional Bodies (FSRBs), which then release Mutual Evaluation Reports (MERs).

- For the countries that don't perform well on certain standards, time-bound action plans are drawn up.

- Recommendations for countries range from assessing risks of crimes to setting up legislative, investigative and judicial mechanisms to pursue cases of money laundering and terror funding.

What are FATF’s ‘grey’ and ‘black’ lists?

- While the words ‘grey’ and ‘black’ list do not exist in the official FATF lexicon, they designate countries that need to work on complying with FATF directives and those who are non-compliant, respectively.

- At the end of every plenary meeting, FATF comes out with two lists of countries.

Grey List

- The grey countries are designated as “jurisdictions under increased monitoring”, working with the FATF to counter criminal financial activities. For such countries, the watchdog does not tell other members to carry out due-diligence measures vis-a-vis the listed country but does tell them to consider the risks such countries possess. Currently, 23 countries including Pakistan are on the grey list.

Black List

- For the black list, it means countries designated as ‘high-risk jurisdictions subject to call for action’.

- In this case, the countries have considerable deficiencies in their AML/CFT (anti-money laundering and counter terrorist financing) regimens. Thus, FATF calls on members and non-members to apply enhanced due diligence.

- In the most serious cases, members are told to apply counter-measures such as sanctions on the listed countries. Currently, North Korea and Iran are on the black list.

- Being listed under the FATF’s lists makes it hard for countries to get aid from organizations like the International Monetary Fund (IMF), Asian Development Bank (ADB), and the European Union. It may also affect capital inflows, foreign direct investments, and portfolio flows.

https://epaper.thehindu.com/Home/ShareArticle?OrgId=GF79TREN6.1&imageview=0

1.png)