The government is planning to blend 15 per cent green hydrogen with piped natural gas (PNG) for domestic, commercial and industrial consumption.

Development for GST

The introduction of the Goods and Services Tax (GST) was made possible by the fact that the state has waived almost all of its authority to collect indirect taxes at the local level and has agreed to fall under the GST framework.

To eliminate the possibility of a state's revenue shortfall, it was agreed that the revenue shortfall due to the transition to the new indirect tax system would be covered by the GST Compensation Fund, which was covered by a compensation tax on some "sin" products.

Revenue loss calculations are made by calculating the difference between the revenue forecast based on cumulative 14% growth from revenue in the base year (2015-2016) and the actual GST survey for the

This compensation b to June 2022.

Compensation Cess Fund:

A compensation fund is created from which the state would be paid the shortfall. An additional levy will be levied on certain items used to pay compensation.

Items include pan masala, tobacco and tobacco products, carbonated water, caffeinated beverages, charcoal, and certain passenger cars.

The GST Act provides that the income collected and "other amounts that may be recommended by the [GST] Council" are credited to the

State Arguments:

States points out that the gap between actual and guaranteed income in recent years is widening.

Their claim is that the COVID 19 pandemic will reduce state revenues and the state will have to spend quite a lot of money to deal with ongoing public health emergencies and their socio-economic implications.

This puts a serious financial burden and leads to the need to increase GST coverage

The state claims that at the time the GST was introduced, the state agreed to waive tax autonomy, guaranteed by the federal government to protect revenues. Therefore, the federal government needs to ensure this by expanding GST coverage.

Way Forward:

Given that the state's financial stress can adversely affect India's post-pandemic economic recovery, the Union Government strongly recommends extending the GST compensation system beyond the current deadline.

Previously, the funds of the GST Compensation Fund were insufficient to cover the loss of income, so the union government borrowed 159 million rupees and gave it to the state and UT.

Instead of such an extraordinary process, the federal government can now apply for amendments to the GST Act to expand the GST compensation system.

To raise funds for the extension, the state can extend the coverage period. It is worth noting that the leveling tax is still being collected well beyond this fiscal year, as the borrowed loan must be paid in lieu of the lack of funds in the leveling fund.

About GST:

GST is known as the Goods and Services Tax.

It is an indirect tax, which has replaced many indirect taxes in India such as the excise duty, VAT, services tax, etc.

The Goods and Service Tax Act was passed in the Parliament on 29th March 2017 and came into effect on 1st July 2017.

Goods and Services Tax Law in India is a comprehensive, multi-stage, destination-based tax that is levied on every value addition. GST is a single domestic indirect tax law for the entire country.

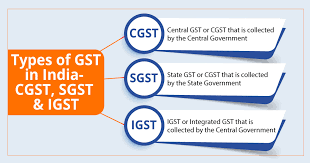

Under the GST regime, the tax is levied at every point of sale. In the case of intra-state sales, Central GST and State GST are charged. All the inter-state sales are chargeable to the Integrated GST.