Description

Disclaimer: Copyright infringement not intended.

Context

- Pakistan announced that the government would introduce interest-free banking in the country.

Interest-Free Banking

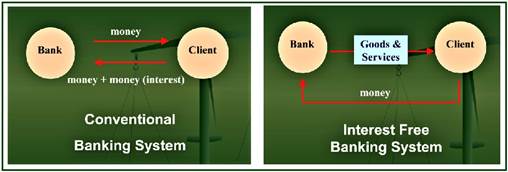

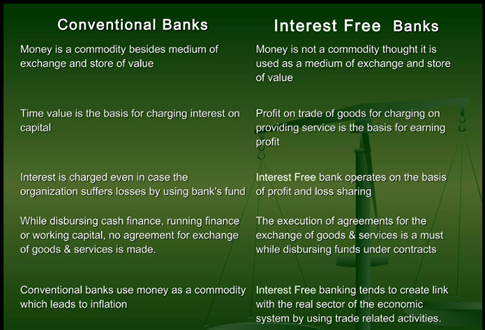

- “Interest-Free Banking” is a fundamental concept derived from the Islamic form of banking. It operates with primitive professional and ethical standards that exclude the “Muslims” from paying or receiving any kind of interest.

- Interest-Free Banking was introduced in Muhammad Zia-ul-Haq regime in the 80s. Since then, it has developed very rapidly.

- Riba is the Islamic term for interest charges on loans, and according to the current interpretation, covers all interest — not just excessive interest. Under Islamic law, a Muslim is prohibited from paying and accepting interest on a predetermined rate.

- As per Islamic banking, money can only be parked in a bank without interest and cannot be used for speculative trading, gambling, or trading in prohibited commodities such as alcohol or pork.

Basis of the Interest-Free Banking Theory

- This theory is based on the knowledge and application of the injunctions of Sharia which prevent injustice.

- Interest-free financial system permits return obtained in the form of profit by investment and business activities that actually produce wealth. It also circulates this wealth in society as widely as possible. The system forbids interest which concentrates wealth in a few hands.

- Interest-free Banking and Finance endeavored in the early sixties in Egypt. Now it has entered into a significant mode and gained a large amount of popularity throughout the globe in twenty-first century with force.

- Interest-Free Banking and Finance endures with conventional banking and finance. Interest-free banking and finance are currently practiced through two means – firstly, Interest-free Banks/Financial Institutions, and secondly, Islamic windows offered by some renowned conventional banks.

How can a bank work without levying interest?

- Interest-Free Banking certainly does not mean that revenue-generating activities or money-raving businesses are not encouraged. All of these business forms are greatly appreciated as far as they do not involve an interest of any kind. There are a lot of financial tools introduced by Islamic financial bodies to fulfil these business or profit-making requirements.

- For a clear understanding, they deal with equity financing rather than reflecting on debt financing. In addition, as a replacement for fixed interest rates on the savings account, these interest-free banks give a small percentage of return on deposits on an annual basis.

Instruments to generate money

Various instruments are available for those who want to take credit from a Sharia-compliant bank.

- In an Ijarah contract, a bank purchases the asset on behalf of the client and allows its usage for a fixed rental rate. After a mutually agreed time, the ownership of the asset is transferred to the client.

- Another instrument is Murabaha, which means a sale on mutually agreed profits. In this financing technique, an asset is purchased by the bank at a market price and sold to the customer at a mutually-decided marked-up cost. The client is allowed to repay in installments.

- Musharaka refers to a joint investment by the bank and the client. Under the agreement, an Islamic bank provides funds, which are mixed with the funds of the business enterprise and others. The bank and the client both contribute to the funding of an investment of purchase, and agree to share the profit or loss in agreed-upon proportions.

- Thus, Islam prohibits interest, not trade. Islamic banks don’t lend money. They operate as trading and investment houses.

Interest-free banking in India

- In a report submitted to the government in 2008, a committee headed by Raghuram Rajan had, without naming Sharia banking, suggested the need to have interest-free banking in India.

- The Reserve Bank of India (RBI) in 201d suggested that given the complexities of Islamic finance and various regulatory challenges involved, Islamic banking could be gradually introduced through the opening of an “Islamic window” in conventional banks.

Final Thought

- While interest-free deposits strengthen banks' financial arm, high inflation can erode the value of the depositors' money since they are not earning interest.

https://indianexpress.com/article/explained/explained-global/what-interest-free-banking-recently-given-green-light-pakistan-8263431/