Description

Disclaimer: Copyright infringement not intended.

Context

- The Reserve Bank of India (RBI) announced a standard operating procedure (SOP) for interoperable regulatory sandbox to regulate newer fintech products and services falling in the ambit of more than one regulator.

Background

- In the world of digital innovation, FinTechs are innovating products in digital payments and lending, e-KYC, credit rating, etc.

- These FinTech innovations are important but the biggest challenge for the regulator is to strike a balance between innovation and regulation.

- The regulator can’t be too strict as it would kill the spirit of innovation and enterprise; it can’t give too much leeway either if it wants to safeguard consumer interest.

Regulatory Sandbox

- A regulatory sandbox is a framework set up by a regulator that allows FinTech startups and other innovators to conduct live experiments in a controlled environment under a regulator’s supervision.

- RBI’s framework for a regulatory sandbox outlines a ‘learning by doing’ approach for all ecosystem players. With certain safeguards, the regulator allows start-ups/Fintechs/tech companies/banks to innovate their products. Regulatory sandbox allows a few cohorts with a limited number of entrants to test their product.

- A regulatory sandbox is live testing of new products or services on a pilot basis with some regulatory relaxations for the limited purpose of the testing. In this regulator may (or may not) permit certain regulatory relaxations for the limited purpose of the testing.

- The RS allows the regulator, the innovators, the financial service providers and the customers to conduct field tests to collect evidence on the benefits and risks of new financial innovations, while carefully monitoring and containing their risks.

|

List of innovative products/services/technology which could be considered for testing under RS are as follows.

Innovative Products/Services

Retail payments

Money transfer services

Marketplace lending

Digital KYC

Financial advisory services

Wealth management services

Digital identification services

Smart contracts

Financial inclusion products

Cyber security products

Innovative Technology

Mobile technology applications (payments, digital identity, etc.)

Data Analytics

Application Program Interface (APIs) services

Applications under block chain technologies

Artificial Intelligence and Machine Learning applications

.

|

Objectives

- The RS provides an environment to innovative technology-led entities for limited-scale testing of a new product or service that may involve some relaxation in a regulatory requirement before a wider-scale launch.

- The RS is, at its core, a formal regulatory programme for market participants to test new products, services or business models with customers in a live environment, subject to certain safeguards and oversight.

Regulatory Sandbox: Benefits

The setting up of an RS can bring several benefits, some of which are significant and are delineated below:

Evidence on benefits and risks of product

- First and foremost, the RS fosters ‘learning by doing’ on all sides. Regulators obtain first-hand empirical evidence on the benefits and risks of emerging technologies and their implications. This enables them to take a considered view on the regulatory changes or new regulations that may be needed to support useful innovation, while reducing the risks.

- Incumbent financial service providers, including banks, also improve their understanding of how new financial technologies might work, which helps Banks to appropriately integrate such new technologies with their business plans.

- Innovators and FinTech companies can improve their understanding of regulations that govern their offerings and shape their products accordingly.

- Finally, feedback from customers, as end users, educates both the regulator and the innovator as to what costs and benefits might accrue to customers from these innovations.

Helps check Viability of product before wide scale roll out

- Users of an RS can test the product’s viability without the need for a larger and more expensive roll-out. If the product appears to have the potential to be successful, the product might then be authorized and brought to the broader market more quickly.

- If any concerns arise, during the sandbox period, appropriate modifications can be made before the product is launched in the broader market.

Helps in financial inclusion

- FinTechs provide solutions that can further financial inclusion in a significant way. The RS can go a long way in not only improving the pace of innovation and technology absorption but also in financial inclusion and in improving financial reach.

- Areas that can potentially get a thrust from the RS include microfinance, innovative small savings and micro-insurance products, remittances, mobile banking and other digital payments.

Enables evidence-based regulatory decision-making

- By providing a structured and institutionalized environment for evidence-based regulatory decision-making, the dependence of the regulator on industry/stakeholder consultations only is correspondingly reduced.

Reduced costs and improved access to financial services

- RS could lead to better outcomes for consumers through an increased range of products and services, reduced costs and improved access to financial services.

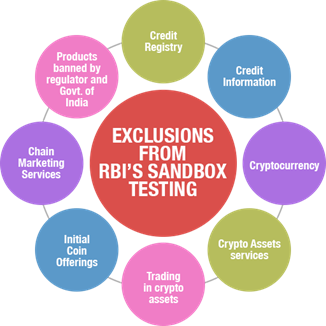

Interoperable Regulatory Sandbox

- Interoperable regulatory sandbox is to test newer fintech products and services falling in the ambit of more than one regulator.

- The move is aimed at developing a clear jurisdiction where there are overlapping areas involving multiple regulators, including the RBI, Securities and Exchange Board of India (Sebi), Insurance Regulatory and Development Authority (Irdai), Pension Fund Regulatory and Development Authority (PFRDA).

- Under the framework, the dominant feature of the product will determine the influence of the regulator and the regulator under whose jurisdiction such feature will be the principal regulator and others will be associate regulators.

|

Determination of Dominant Feature

Two sets of factors would be considered on deciding the dominant feature. Firstly, the type of enhancement to the existing products like loans, deposits, capital market instruments, insurance, G-sec instruments and pension products. And secondly, the number of relaxations sought by the entity for undertaking the test under the IoRS. The dominant feature would be decided with greater weightage to the number of relaxations sought.

|

- The test design will be finalised by the principal regulator in consultation with other regulators. The fintech selected for the sandbox will seek permission of the principal regulator for relaxations before launching the product.

- The relaxation, if warranted, would be considered by the principal and associate regulator on case-to-case basis and decision to that effect would be binding and final.

Special cases

- In cases where SEBI is involved, a fintech applicant not registered with the markets regulator will have to partner with SEBI registered entity under its norms.

- Separately, International Financial Services Centres Authority (IFSCA) will be the principal regulator in cases where Indian fintech is looking to launch products abroad or foreign fintechs planning to initiate products in India.

A Global Perspective

- A regulatory sandbox was first implemented by the United Kingdom in 2015 and since then other countries have been quick to implement regulatory sandbox framework to suit their varying needs.

- In 2016, the Monetary Authority of Singapore (MAS) had initiated the process of building a framework around Sandbox. So far MAS has engaged with more than 150 FinTech players since the launch of sandbox and a number of firms have experimented their innovations in the sandbox.

- In 2017, the Australian Securities & Investment Commission (ASIC) had come up with waivers allowing FinTechs to test services as per guidelines for up to 12 months without having an Australian financial service or credit license.

- In June 2017, Bahrain came with a FinTech sandbox allowing FinTechs to test their innovations in specific categories for nine months without any major regulation.

The way forward

- Ultimately, when considering both risk and reward, the singular policy goal should be abundantly clear: set common principles and National legal standards in order steer the path towards cross-sandbox interoperability.

- Solid cross-jurisdictional cooperation is the best way to mitigate the risks of ‘regulatory arbitrage,’ or the creation of confronted competing ‘factions’.

https://www.financialexpress.com/economy/rbi-announces-sop-for-interoperable-regulatory-sandbox/2708468/