Recently, government has initiated further proceedings for the sale of BPCL.

Evolution for Privatisation:

The balance of payment (BoP) crisis in early 1990s changed the official narrative about PSUs — from “temples of modern India” to “the government has no business to be in business”.

In order to bring the economy back on track, the PV Narasimha Rao government (June 21, 1991- May 16, 1996) launched economic reforms by ending the era of license-quota raj and encouraging privatisation.

The Atal Bihari Vajpayee government classified PSUs into two categories — strategic and non-strategic — and decided to gradually to offload its stake in non-strategic firms.

To have a focused approach, a Department of Disinvestment was set up on December 10, 1999, which was later renamed as the Ministry of Disinvestment form September 6, 2001.

The budget (2000-01), for the first time, used the word privatisation along with disinvestment.

In 2001, The government approved privatisation of 27 companies. These companies include among others VSNL, Air India, and Maruti Udyog Ltd.

Between 2001 and 2004, India saw disinvestments of government’s stake in several companies, including strategic sale of Bharat Aluminium Co Ltd, CMC Ltd, Hindustan Zinc Ltd, three properties of HCI, 18 properties of ITDC, Indian Petrochemicals Corp Ltd (IPCL) and Paradeep Phosphates Ltd.

In November 2007, the government constituted the National Investment Fund (NIF) into which the proceeds from disinvestment of government equity in central public sector enterprises (CPSEs) were deposited. It was said that three-quarters of annual income of the fund would be used to finance select social sector schemes that promote education, health and employment.

Current Policy is no longer limited to strategic sale or dilution of government’s minority stake in the company. It also included monetisation of assets owned by CPSEs.

Disinvestment Commission Under GV Ramakrishna:

The essence of a long-term disinvestment strategy should be not only to enhance budgetary receipts, but also minimise budgetary support towards unprofitable units while ensuring their long-term viability and sustainable levels of employment in them.

Need for Privatisation:

Need to push for privatisation so that there is overall enhancement of total factor productivity. It will ensure growth at high rates on a sustained basis.

Enhance Gross Capital Formation:To enhance gross capital formation enhanced participation of the private sector is must.

privatisation push is based on the rationale of bad performance by these PSUs and therefore, they need private sector support to survive.

Economic Survey has highlighted thatseveral areas from banking to cement and steel where opening up the sectors to private players has led to massive efficiency gains, increased profitability, improved return on assets, and better access and service to customers.

According to the Economic Survey, A comparative analysis of the before-after performance of 11 CPSEs that went through strategic disinvestment reveals that net worth, net profit, return on assets, return on equity, gross revenue, net profit margin, sales growth and gross profit peremployee of the privatised CPSEs, on an average, have improved significantly in the post privatization period compared to the peer firms

Strategic sale of majority stake to private players produced much better results, indicating its preference for privatisation of government-owned companies.

Increased Borrowing by the Government: The gap between the government’s income and expenditure shot up from Rs 7.96 lakh crore to Rs 18.48 lakh crore and is expected to be capped at Rs 15.06 lakhthe level of borrowings and deficit will hurt cost competitiveness and economic growth. To pave a path towards a low-cost high-growth economy, the government must cut its borrowings and shrink debt and deficit levels. And the moolah mantra is obviously privatisation.

Monetisation of Assets:Privatisation affords the monetisation of assets, caps erosion of public wealth, frees resources for human and physical infrastructure and promises the upside of enhanced growth as enterprise productivity improves.

Challenges with the Privatisation:

It will lead to monopoly over the important shared resources of the public.

Sale of profit-making and dividend paying PSUs would result in the loss of regular income to the Government

There would be chances of “Asset Striping” by the strategic partner. Most of the PSUs have valuable assets in the plant and machinery, land and buildings, etc.

Strategic and National Security Concerns: Strategic Disinvestment of Oil PSUs is seen by some experts as a threat to National Security since Oil is a strategic natural resource and possible ownership in the foriegn hand is not consistent with our strategic goals.

Disinvestment affects labour forces' social security.

It also raises concerns about cronyism.

The depressed state of the markets and the paucity of reasonable buyers would land in a bad deal.

Using funds from disinvestment to bridge the fiscal deficit is an unhealthy and a short term practice. It is said that it is the equivalent of selling 'family silver' to meet short term monetary requirements.

About Strategic Disinvestment:

Strategic disinvestment would imply the sale of substantial portion of the Government share holding of a central public sector enterprise (CPSE) of upto 50%, or such higher percentage as the competent authority may determine, along with transfer of management control.

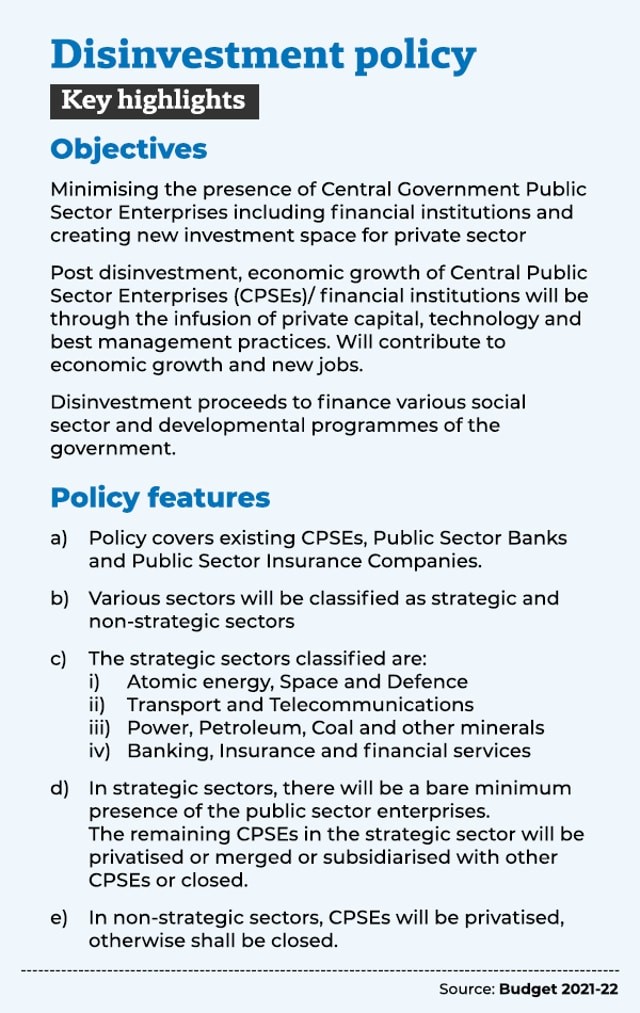

New Public Sector Enterprise Policy:

Under the New Policy:

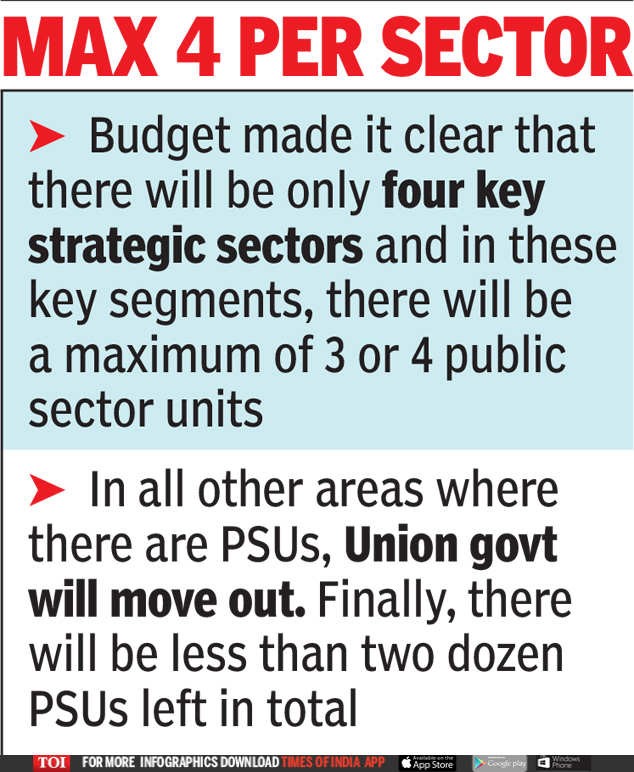

Strategic: Atomic energy, space, defence, trans and telecom, power, petro, coal, other minerals, banking, insurance and financial services will be classified as strategic sectors.

Privatization: The remaining companies in strategic sectors will be considered for privatization/merger/closure and non-strategic sectors will be considered for privatization, where feasible or for closure.

In strategic sectors, the minimum presence of existing companies at the holding level will be retained under government control.

The strategic sectors have limited number of players restricting it to maximum four public sector enterprises of the holding nature.

NITI has been asked to work out on the next list of Central Public Sector companies that would be taken up for strategic disinvestment.

Current Status:

The government has already set in motion privatisation plans for large PSU companies BPCL, Air India, Container Corporation of India, and Shipping Corporation of India.