Account Aggregators: New framework to access, share financial data

Figure 2: No Copyright Infringement Intended

Context:

- On September 2 eight of India’s major banks — State Bank of India, ICICI Bank, Axis Bank, IDFC First Bank, Kotak Mahindra Bank, HDFC Bank, IndusInd Bank and Federal Bank — joined the Account Aggregator (AA) network that will enable customers to easily access and share their financial data.

About Account Aggregators:

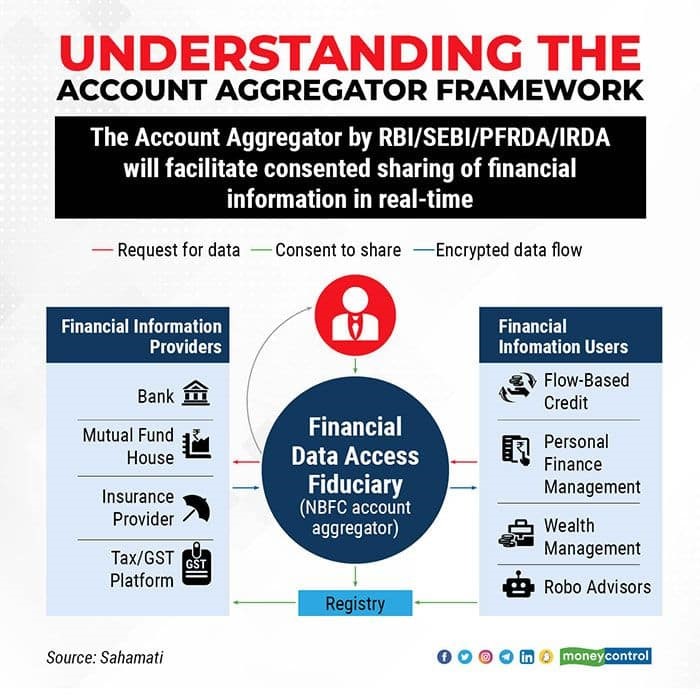

- According to the Reserve Bank of India, an Account Aggregator is a non-banking financial company engaged in the business of providing, under a contract, the service of retrieving or collecting financial information pertaining to its customer.

- It is also engaged in consolidating, organising and presenting such information to the customer or any other financial information user as may be specified by the bank.

About Account Aggregator Framework:

- The licence for AAs is issued by the RBI, and the financial sector will have many AAs.

- The AA framework allows customers to avail various financial services from a host of providers on a single portal based on a consent method, under which the consumers can choose what financial data to share and with which entity.

Function of Account Aggregator:

- It reduces the need for individuals to wait in long bank queues, use Internet banking portals, share their passwords, or seek out physical notarisation to access and share their financial documents.

- An Account Aggregator is a financial utility for secure flow of data controlled by the individual.

- This will help banks reduce transaction costs, which will enable us to offer lower ticket size loans and more tailored products and services to our customers.

- It will also help us reduce frauds and comply with upcoming privacy laws.

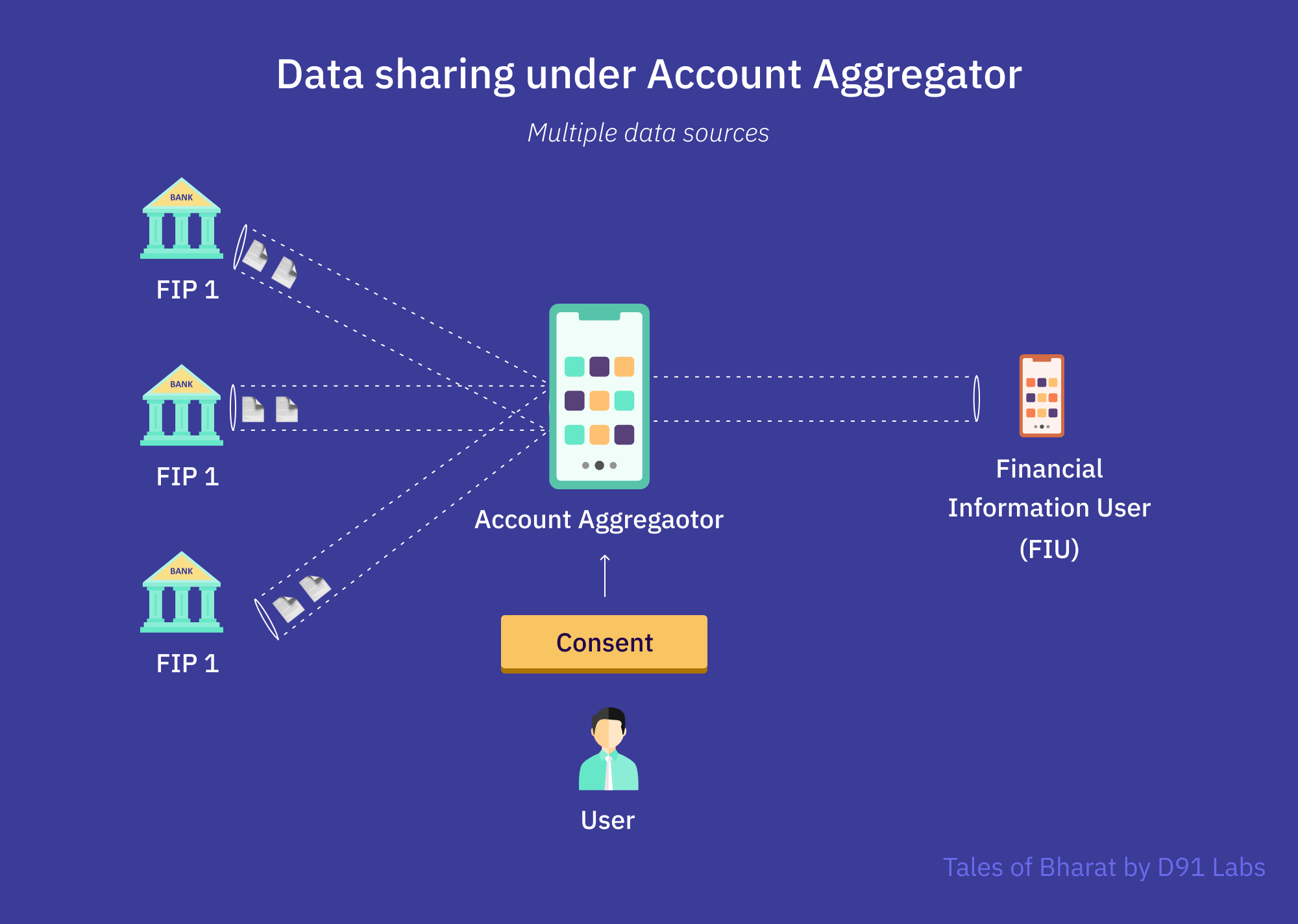

Working of Account Aggregator:

- It has a three-tier structure: Account Aggregator, FIP (Financial Information Provider) and FIU (Financial Information User).

- An FIP is the data fiduciary, which holds customers’ data. It can be a bank, NBFC, mutual fund, insurance repository or pension fund repository.

- An FIU consumes the data from an FIP to provide various services to the consumer.

- An FIU is a lending bank that wants access to the borrower’s data to determine if the borrower qualifies for a loan. Banks play a dual role – as an FIP and as an FIU.

Sharing of Data:

- An Account Aggregator allows a customer to transfer his financial information pertaining to various accounts such as banks deposits, equity, mutual fund and pension funds to any entity requiring access to such information.

- There are 19 categories of information that fall under ‘financial information’, besides various other categories relating to banking and investments.

About Data Storage Provisions:

- Data transmitted through the AA is encrypted.

- AAs are not allowed to store, process and sell the customer’s data. No financial information accessed by the AA from an FIP should reside with the AA.

- It should not use the services of a third-party service provider for undertaking the business of account aggregation.

1.png)