Disclaimer: Copyright infringement not intended.

Context

Findings

|

Macroeconomic Fundamentals Macroeconomic fundamentals are topics that affect an economy at-large, including statistics regarding unemployment, supply and demand, growth, and inflation, as well as considerations for monetary or fiscal policy and international trade. |

|

Incremental CD ratio (ICDR) Incremental CD ratio (ICDR) – is the ratio of change in credit year–on–year to the change in deposit year–on–year. It is the portion of deposits that the banks use to extend loans. The ratio is an indication of the bank's dependence on borrowed funds to fund its credit growth. If the incremental CD ratio increases beyond 100% then the credit growth is outstripping growth in deposit. A loan-to-deposit ratio of 100% means a bank loaned one dollar to customers for every dollar received in deposits it received. It also means a bank will not have significant reserves available for expected or unexpected contingencies. In a nutshell, if CDR is to low: banks may not be earning as much as they should and it also indicates that banks are not mobilizing their resources fully. If the ratio is too high: it means that banks might not have enough liquidity to cover any unforeseen fund requirements, which may cause an asset-liability mismatch. Typically, the ideal loan-to-deposit ratio is 80% to 90%. |

.jpg)

|

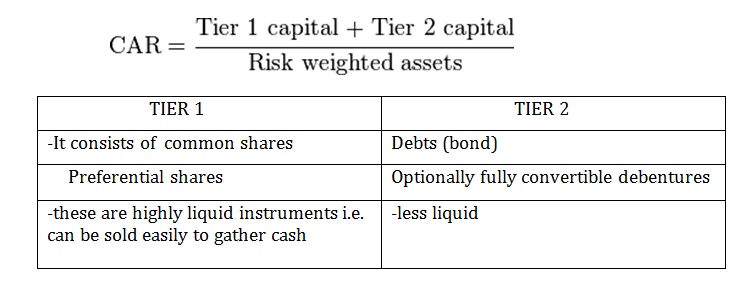

Capital Adequacy Ratio (CAR) Capital Adequacy Ratio (CAR) is also known as Capital to Risk (Weighted) Assets Ratio (CRAR), is the ratio of a bank's capital to its risk. National regulators track a bank's CAR to ensure that it can absorb a reasonable amount of loss and complies with statutory Capital requirements. Description: It is measured as Capital Adequacy Ratio = (Tier I + Tier II + Tier III (Capital funds)) /Risk weighted assets The risk weighted assets take into account credit risk, market risk and operational risk. Tier 1 capital is the primary funding source of the bank. Tier 1 capital consists of shareholders' equity and retained earnings. Tier 1 capital represents the core equity assets of a bank or financial institution. It is largely composed of disclosed reserves (also known as retained earnings) and common stock. The term tier 2 capital refers to one of the components of a bank's required reserves. Tier 2 is designated as the second or supplementary layer of a bank's capital. Tier 2 capital includes revaluation reserves, hybrid capital instruments and subordinated term debt, general loan-loss reserves, and undisclosed reserves. Tier 3 capital is tertiary capital, which many banks hold to support their market risk, commodities risk, and foreign currency risk, derived from trading activities. Tier 3 capital includes a greater variety of debt than tier 1 and tier 2 capital but is of a much lower quality than either of the two. The Basel III norms stipulated a capital to risk weighted assets of 8%. However, as per RBI norms, Indian scheduled commercial banks are required to maintain a CAR of 9% while Indian public sector banks are emphasized to maintain a CAR of 12%. |

Read about NPA: https://www.iasgyan.in/daily-current-affairs/non-performing-assets#:~:text=NPA%20or%20Non%20Performing%20Assets,Non%20Performing%20Assets%20or%20NPA

Read all about NBFC: https://www.iasgyan.in/blogs/nbfcs-and-its-types

© 2025 iasgyan. All right reserved